DSCR loan qualification offers real estate investors a streamlined path to finance income-producing properties. Unlike traditional mortgages that demand extensive personal income verification, these loans prioritize your property’s cash flow, making them ideal for rentals. This guide explains how to qualify for a DSCR loan in 2025, covering key steps and pitfalls to avoid.

Introduction to DSCR Loan Qualification

As a real estate investor, you understand the value of leveraging debt to expand your portfolio. Navigating financing options can be complex, but learning how to qualify for a DSCR loan simplifies the process for income-producing properties. These loans focus on the property’s revenue rather than your personal income, offering flexibility for investors. To learn more about what a DSCR loan entails, see our DSCR Loan Meaning guide.

Qualifying for a DSCR loan requires meeting specific lender criteria to ensure profitability. This guide details the essentials of how to qualify for a DSCR loan, including income rules, critical ratios, and red flags that could block approval. For deeper insights, check our DSCR Loan Requirements guide. Whether you’re seasoned or starting out, mastering how to qualify for a DSCR loan is key to securing funds.

What is a DSCR Loan?

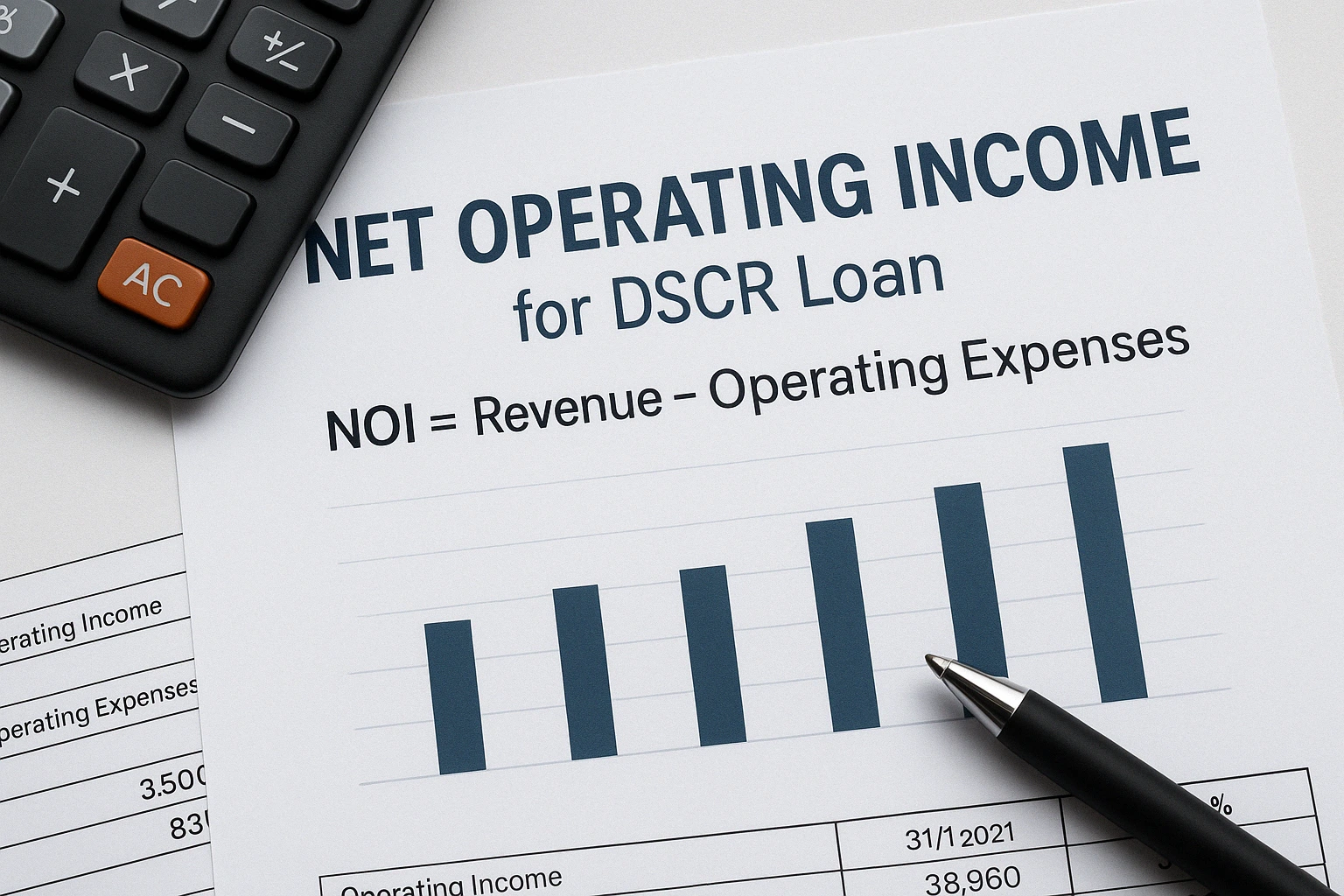

A DSCR loan (Debt Service Coverage Ratio loan) assesses a property’s income potential over personal earnings, making it easier to understand how to qualify for a DSCR loan. The DSCR ratio measures Net Operating Income (NOI) against total debt service (principal, interest, taxes, insurance—PITI). For a deeper dive into the DSCR formula, check Investopedia’s DSCR guide. They are especially useful for short-term rentals, like Airbnb properties; see our short-term rental loans guide for details.

Knowing how to qualify for a DSCR loan means focusing on the property’s ability to generate income. These loans are ideal for investors who want to scale their portfolios efficiently, including those exploring options like mixed-use property financing.

The DSCR Formula

DSCR = Net Operating Income (NOI) / Total Debt Service (PITI)

- Net Operating Income (NOI): Property revenue (e.g., rent) minus operating expenses like management fees, maintenance, insurance, taxes, and vacancy allowances, excluding debt service.

- Total Debt Service (PITI): Monthly loan costs, covering principal, interest, property taxes, and hazard insurance.

- Why It Matters: Understanding this formula is critical to learning how to qualify for a DSCR loan.

Why are DSCR Loans Popular?

- Simplified Verification: Minimal personal income documentation benefits self-employed or complex-income investors.

- Property-Centric: Approval depends on the property’s debt coverage, easing financing for strong rentals.

- Portfolio Growth: Less focus on personal debt-to-income ratios enables faster property acquisitions.

- Rental Fit: Tailored for income-generating properties, ideal for buy-and-hold investors.

- Flexible Income: Properties can qualify based on rental revenue, with stricter criteria than past NINJA loans.

Key Factors for DSCR Loan Qualification

Understanding how to qualify for a DSCR loan hinges on factors beyond personal income, assessing investment risk. Choosing the right lender matters, as terms vary, so researching how to apply for a DSCR loan is essential. For a step-by-step process, see our guide on how to get a DSCR loan. Here’s what you need to know to master how to qualify for a DSCR loan:

1. Debt Service Coverage Ratio (DSCR)

The DSCR is central to how to qualify for a DSCR loan. Lenders typically want a ratio of 1.0 or higher, where NOI equals or exceeds debt service.

- DSCR > 1.0: Indicates surplus income to cover debt and contingencies, favored by lenders.

- DSCR = 1.0: Shows breakeven income, riskier but sometimes accepted.

- DSCR < 1.0: Signals insufficient income, rarely approved without strong assets, making it a hurdle in how to qualify for a DSCR loan.

Example:

- NOI: $2,000 per month

- PITI: $1,500 per month

- DSCR: $2,000 / $1,500 = 1.33

A 1.33 DSCR is strong, enhancing approval chances.

2. Loan-to-Value Ratio (LTV)

The LTV ratio, comparing loan amount to property value, is crucial for DSCR loan qualification. Lower ratios reduce lender risk.

- LTV Calculation: Loan Amount / Property Value

- Typical Range: 65% – 80%, needing a 20% – 35% down payment.

- Rate Impact: Lower LTVs often yield better rates.

3. Credit Score

Credit scores play a role in DSCR loan eligibility, though less than in traditional loans. A solid score reflects financial responsibility.

- Minimum Scores: Usually 620-680; lower scores may mean higher rates.

- Score Effects: Higher scores secure better terms.

- History Review: Includes checks for bankruptcies or late payments.

4. Property Type and Condition

Rentable, well-maintained properties are essential for qualifying for a DSCR loan.

- Types: Single-family, 2-4 unit multifamily, condos, townhomes; some cover larger properties.

- Condition: Requires appraisals or inspections; major repairs can halt approval. Location: High-demand areas are preferred.

5. Appraisal

An appraisal verifies property value, supporting DSCR loan qualification.

- Valuation: Ensures the loan matches the investment’s worth.

- Contingency: Protects against low appraisals.

- Challenges: Dispute inaccuracies with comparable sales.

6. Reserves

Cash reserves bolster DSCR loan eligibility by showing financial stability.

- Requirements: 3-12 months of PITI, depending on the lender.

- Sources: Savings, stocks, or liquid assets.

- Purpose: Covers vacancies or repairs, lowering default risk.

7. Experience (Varies by Lender)

Some lenders consider experience in DSCR loan qualification.

- Experience Benefits: Rental management success aids approval.

- New Investors: Strong credit or reserves offset limited experience.

Income Rules for DSCR Loan Qualification

Understanding Net Operating Income (NOI) calculations is vital for learning how to qualify for a DSCR loan. Here’s a detailed look at income rules to help you master how to qualify for a DSCR loan:

1. Calculating Net Operating Income (NOI)

NOI, the property’s revenue minus expenses (excluding debt service), drives how to qualify for a DSCR loan.

Included in Revenue:

- Gross Rental Income: Total tenant rent, a key factor in how to qualify for a DSCR loan.

- Other Income: Fees like laundry or parking.

Included in Operating Expenses:

- Management Fees: Costs for property oversight.

- Maintenance: Upkeep expenses, e.g., plumbing or landscaping.

- Insurance: Property premiums.

- Taxes: Local property taxes.

- Vacancy Allowance: 5-10% of rent for vacant periods.

- HOA Fees: If applicable, association dues.

Excluded from Operating Expenses:

- Debt Service (PITI): Calculated separately.

- Depreciation: Non-cash expense, omitted.

- Capital Expenditures: Major renovations, not included.

Example NOI Calculation:

- Gross Rental Income: $2,500 per month

- Vacancy Allowance (5%): $125 per month

- Property Management Fees (10%): $250 per month

- Repairs and Maintenance: $100 per month

- Insurance: $100 per month

- Property Taxes: $200 per month

- NOI = $2,500 – $125 – $250 – $100 – $100 – $200 = $1,725 per month

Accurate NOI calculations are essential for how to qualify for a DSCR loan.

2. Importance of Accurate Rental Income

Precise rental income is crucial for qualifying for a DSCR loan. To verify income, provide:

- Lease Agreements: Confirm current rents.

- Rent Roll: Summarize tenant and lease details.

- Market Analysis: Align income with local rates.

Market vs. Actual Rents:

- Vacant Units: Use market rents for estimates.

- Below-Market: Assume potential rent increases.

- Above-Market: Apply conservative market rates.

3. Calculating Total Debt Service (PITI)

PITI covers monthly loan costs, essential for DSCR calculations:

- Principal: Loan balance payment.

- Interest: Monthly interest charge.

- Taxes: Monthly portion of annual taxes.

- Insurance: Monthly premiums.

Accurate tax and insurance quotes ensure reliable PITI figures.

Red Flags That Can Derail DSCR Loan Qualification

A strong DSCR isn’t enough if red flags arise. Mitigate these to boost how to qualify for a DSCR loan successfully:

1. Low DSCR

A DSCR below 1.0 indicates insufficient income, a major hurdle in how to qualify for a DSCR loan.

Solutions:

- Increase Rents: Raise rents to boost NOI, helping how to qualify for a DSCR loan.

- Reduce Costs: Cut fees like management or insurance.

- Bigger Down Payment: Lower the loan to reduce PITI.

- Better Property: Choose assets with stronger income.

2. High Vacancy Rates

Frequent vacancies suggest rental or property issues, complicating how to qualify for a DSCR loan.

Solutions:

- Address Issues: Fix maintenance or location problems.

- Improve Marketing: Attract tenants with better strategies.

- Lower Rents Temporarily: Fill units quickly.

- Show Plans: Present a vacancy reduction strategy.

3. Significant Deferred Maintenance

Poor property condition raises repair cost concerns, impacting how to qualify for a DSCR loan.

Solutions:

- Make Repairs: Fix issues pre-application.

- Estimate Costs: Provide repair budgets.

- Adjust NOI: Include repair costs in calculations.

4. Unstable Rental Market

Volatile markets complicate income forecasts.

Solutions:

- Research Thoroughly: Study local rental trends.

- Support Projections: Use market rent analyses.

- Emphasize Positives: Highlight rising rents or low vacancies.

5. Borrower Credit Issues

Credit problems can challenge DSCR loan qualification, though less than income issues.

Solutions:

- Boost Credit: Reduce debt or fix report errors.

- Clarify Issues: Explain negative marks.

- Co-Borrower: Partner with stronger credit.

6. Inaccurate Rental Income

Overstated income risks denial.

Solutions:

- Verifiable Records: Submit accurate leases and rent rolls.

- Realistic Estimates: Use market-based projections.

- Openness: Disclose income challenges.

7. Insufficient Reserves

Low reserves signal instability.

Solutions:

- Save More: Build cash reserves.

- Liquidate Assets: Convert investments to cash.

- Other Sources: Consider credit lines for reserves.

Interactive Element: DSCR Calculator

This free calculator helps estimate your DSCR, a key step in how to qualify for a DSCR loan. Try our free calculators, like the Free Advanced Mortgage Calculator, for more insights.

DSCR Calculator

Disclaimer: Results are estimates for how to qualify for a DSCR loan. Consult lenders for exact DSCR.

Tips for Maximizing DSCR Loan Qualification

- Compare Lenders: Shop around for the best rates and terms to learn how to qualify for a DSCR loan. Check our DSCR lenders guide for top options.

- Use a Broker: Brokers simplify finding suitable lenders for how to qualify for a DSCR loan.

- Get Pre-Approved: Strengthen your offers with pre-approval.

- Prepare Documents: Have leases, rent rolls, and statements ready.

- Stay Transparent: Be open about property or financial issues.

- Enhance Management: Show a plan to maximize rental income.

Frequently Asked Questions

Conclusion: Mastering DSCR Loan Qualification

DSCR loan qualification empowers investors to finance rental properties efficiently. By addressing lender criteria, avoiding pitfalls, and preparing thoroughly, you can secure how to qualify for a DSCR loan successfully. Optimize property income, maintain solid credit, and build reserves to succeed. With these steps, you’ll achieve your investment goals through real estate, whether for traditional rentals or specialized properties like financing modular homes.

Don’t Let Cash Flow Kill the Deal

Get Up to $50K in DSCR-Friendly Personal Loans