Looking to invest smarter in 2025? DSCR lenders offer cash-flow-based loans that focus on your property’s income—not your W-2s. If you want speed and fewer docs, this route can help. Sound familiar? To get the full picture of how these loans work and why they matter, check out our dscr loan explained guide. It covers leading cash-flow financing providers, compares their metrics, and shares expert tips to help you choose the right partner to scale your portfolio.

This post contains affiliate links. If you buy through our links, we may earn a commission at no extra cost to you. Learn more.

Table of Contents

- Introduction: Why Cash Flow Lenders Matter in 2025

- What Are DSCR Lenders?

- Quick DSCR Calculator

- Why Cash Flow Lenders Are Key for Investors

- Top DSCR Lenders for 2025

- Comparing Lender Metrics

- How to Choose the Right DSCR Lender for Investment Property Financing

- Methodology

- Mini Case Study

- Expert Analysis

- Key Takeaways

- FAQ Section

- Conclusion & Next Steps

Introduction: Why Cash Flow Lenders Matter in 2025

In today’s fast-paced real estate market, cash-flow lenders have emerged as a go-to solution for investors seeking investment property financing without the burden of extensive income verification. As we head into 2025, the financing landscape is evolving, with traditional lenders tightening requirements and prioritizing owner-occupied properties. This shift has created a gap for real estate investors, making cash-flow loans increasingly critical.

Unlike conventional loans that hinge on personal income, W-2 statements, and debt-to-income ratios, cash-flow lenders focus on a property’s ability to generate rental income. This approach helps investors who might struggle under traditional guidelines, such as those managing multiple properties, self-employed entrepreneurs, or individuals with non-traditional income sources. In 2025, this flexibility is especially valuable as rental demand remains robust, fueled by trends like urbanization, remote work, and a growing preference for renting over homeownership.

Challenges still exist: rising interest rates, potential regulatory changes, and regional market variations. Cash-flow lenders help by offering a streamlined path to capital, enabling investors to move quickly in competitive markets. For example, a property earning $4,000 in monthly rent may qualify based on that cash flow even when personal finances do not fit bank standards. The focus on property performance speeds decisions when deals appear.

This guide explores leading cash-flow financing providers for 2025, how they operate, the metrics that matter, and practical tips for choosing the right partner. Whether you’re looking at single-family rentals, multifamily buildings, or short-term rentals, understanding cash-flow loans can open new doors for your portfolio.

What Are DSCR Lenders?

Cash-flow lenders are financial institutions or private lenders specializing in cash-flow loans that evaluate a real estate investment’s ability to cover its debt obligations. The cornerstone is the Debt Service Coverage Ratio (DSCR), calculated by dividing a property’s net operating income (NOI) by its total debt service (monthly principal and interest payments). In plain terms, DSCR compares a property’s income to its debt payments; above 1.0 means income covers debt. (See definitions in the FAQ)

This cash-flow model sets cash-flow lenders apart from traditional banks, which rely heavily on an individual’s debt-to-income (DTI) ratio and documented income. By prioritizing property performance, DSCR loans make financing more accessible for investors with complex financial profiles, such as those juggling multiple properties or running their own businesses. A landlord with irregular personal income but income-producing rentals may still qualify based on the strength of the properties’ cash flow.

Investment property financing through cash-flow lenders involves trade-offs. Interest rates are typically about 0.5% to 1.5% higher than conventional mortgages, reflecting the added risk of focusing on property income rather than personal creditworthiness. Credit scores and liquidity still matter, but they are secondary to DSCR, which usually must meet a minimum threshold (for example, 1.15 or 1.25). Despite the cost, documentation is streamlined and underwriting can be completed in as little as two weeks, which can keep growth plans on track.

Quick DSCR Calculator

Estimate your DSCR in seconds. Enter your property’s monthly NOI and principal & interest. The meter shows if you’re near common thresholds (1.15–1.25). Use the score to shortlist lenders below.

Green ≥ 1.25, Amber 1.15–1.24, Red < 1.15. Tip: If DSCR is borderline, test small NOI or payment changes.

Why Cash Flow Lenders Are Crucial to Real Estate Investors

Industry reports suggest cash-flow lenders played a growing role in 2024, and that momentum may continue in 2025 as investors seek flexible funding to scale.

For real estate investors, cash-flow lenders align financing with how rental properties actually operate. Approvals often arrive faster than bank loans, strong property income can support larger balances, and programs are flexible enough to include short-term rentals, fix-and-flip projects, and multifamily assets. See DSCR loans for Airbnb for options that factor in seasonal income.

Consider an investor with a multifamily property generating $10,000 in monthly rent. Even if personal income fluctuates, a cash-flow lender prioritizes the property’s cash flow and may approve a larger loan than a traditional bank. With rental demand still strong in 2025, cash-flow loans help investors compete for single-family rentals and large apartment complexes alike.

Top DSCR Lenders for 2025

Below are five noteworthy DSCR lenders poised to lead the market in 2025, each offering a distinct advantage for investors seeking cash-flow loans:

- Skyline Funding Solutions

Known for quick approvals and a streamlined online application, Skyline offers loan-to-value (LTV) ratios up to 80%. They specialize in single-family rentals and small portfolios and can close in about 10–14 days in favorable scenarios. - Pioneer Commercial Bank

Designed for both seasoned investors and newcomers, Pioneer’s DSCR programs feature a minimum DSCR of 1.15. The focus on multifamily properties and thorough underwriting can extend approvals to 3–4 weeks. - Integrity Capital Group

A solid option for short-term rentals and vacation properties. The team considers real-world occupancy for Airbnb and VRBO hosts so terms reflect seasonality in tourist markets. - Evergreen Lending Partners

A private lender for portfolio expansion. Cross-collateralization of multiple properties can secure larger loans, though higher credit scores (700+) are typical. - MetroStar Financing

Pricing is often about 0.25% to 0.50% above conventional loans—aimed at large multifamily deals. Expect detailed property management documentation in exchange for better rates.

Comparing Cash Flow Lenders: Key Metrics

When comparing dscr lenders, details matter. From minimum DSCR to credit score benchmarks, knowing each lender’s metrics helps you target the right fit. To estimate payments for a specific property, try our free Advanced Mortgage Calculator.

| Criteria | Skyline Funding | Pioneer Bank | Integrity Group | Evergreen Lending | MetroStar Financing |

|---|---|---|---|---|---|

| Minimum DSCR | 1.20 | 1.15 | 1.20 | 1.25 | 1.25 |

| Credit Score Minimum | 680 | 650 | 660 | 700 | 680 |

| Max LTV | 80% | 75% | 75% | 80% | 75% |

| Primary Focus | Single-Family & SFR Portfolios | Mixed-Use & Multifamily | Short-Term Rentals | Multi-Property Bundling | Large Multifamily Deals |

| Typical Rates (Approx.) | +1.00% Over Conventional | +1.25% Over Conventional | +1.50% Over Conventional | +1.00% Over Conventional | +0.50% Over Conventional |

While Skyline Funding excels in rapid closings, Pioneer can be more lenient on DSCR. If you’re exploring short-term rentals, Integrity Group is often more flexible in how rental income is calculated.

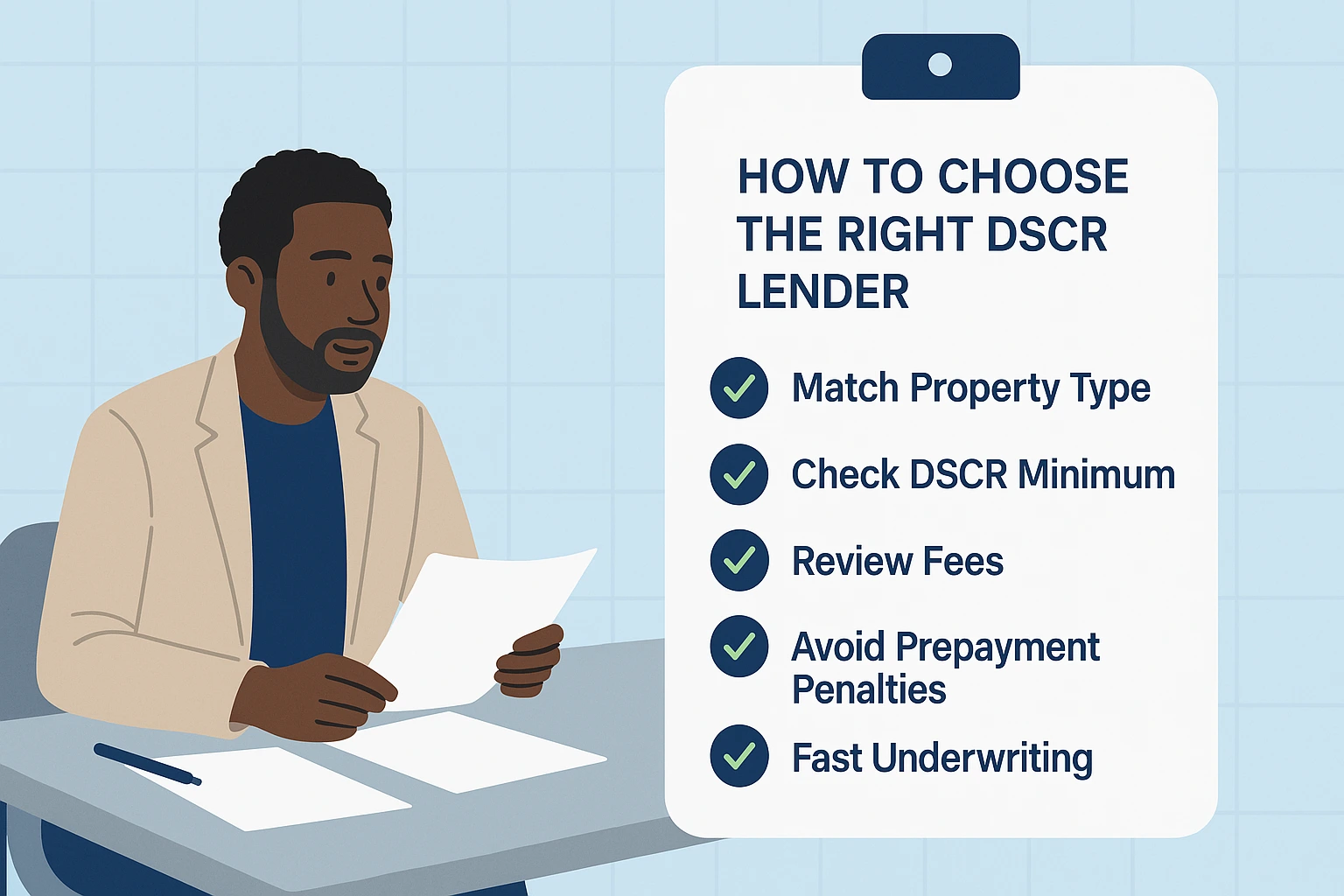

How to Choose the Right DSCR Lender for Investment Property Financing

Selecting the right partner among dscr lenders is about more than interest rates. You want a partner aligned with your strategy. For insights on fees and approval tactics, see what to look for in a DSCR lender.

1. Match the Lender to Your Property Type

Some DSCR lenders specialize in single-family rentals, while others focus on multifamily or commercial properties. Choose lenders experienced with your asset type. For example, Integrity Capital Group often suits short-term rentals, whereas MetroStar fits large multifamily complexes.

2. Assess Minimum DSCR Requirements

If your property is near a 1.15 DSCR, target lenders known to accept lower coverage ratios. You may face higher pricing or tighter terms to offset risk.

3. Evaluate Fees and Closing Costs

DSCR loans typically carry higher origination fees than conventional mortgages. Some lenders charge 1%–2%, while others bundle admin or legal fees. Request a Loan Estimate to understand total cost.

4. Look Into Prepayment Penalties

Many DSCR lenders include prepayment penalties. If you plan to refinance or sell within five years, prioritize low or no penalty structures to preserve flexibility.

5. Check Support and Underwriting Speed for Investment Property Financing

The DSCR process can be swift or slow depending on underwriting. Skyline Funding is known for quick pipelines, helpful when deadlines are tight.

Methodology

We reviewed lender programs publicly available in 2024–2025 and looked for transparent DSCR floors, LTV caps, average timelines, and support for rental types (SFR, multifamily, short-term). Each listing above reflects a typical scenario; final terms depend on credit, reserves, and property performance. We refreshed this page when lenders updated rate sheets or program guides and cross-checked their published DSCR floors and LTV caps against recent rate sheets or program guides where available.

Reviewed: October 2025.

Mini Case Study

A duplex earns $3,900 NOI per month with a proposed $3,100 payment. DSCR = 1.26. That qualifies for lenders with a 1.25 floor (for example, Evergreen and MetroStar) and easily meets 1.20 and 1.15 programs. If the payment rose to $3,300 (DSCR 1.18), options narrow to programs that allow 1.15–1.20 and pricing usually increases by 25–50 bps.

Expert Analysis

Expert Insight: “Choosing a DSCR lender is akin to choosing a long-term partner. It’s not just about the stated interest rate but also the lender’s flexibility and understanding of real estate cycles. When you find a lender who can adapt terms based on your strategy, you give yourself a major competitive advantage.” — Sarah Johnson, Real Estate Portfolio Strategist

Key Takeaways

- Cash flow first: approvals hinge on rental income more than personal income.

- Know your minimum: target lenders whose DSCR floor matches your property.

- Compare broadly: review at least three to five lenders on rate, fees, and timeline.

- Bring documents: leases, occupancy, and expense projections speed underwriting.

- Think ahead: choose terms that keep refinancing and portfolio growth easy.

Frequently Asked Questions

Conclusion & Next Steps

Your DSCR sets the playing field—use the calculator above to gauge fit, then shortlist lenders that match your ratio, property type, and timeline. Gather leases, occupancy, and expense docs before you apply to shave days off underwriting. If you expect to refinance or scale, favor programs with lighter prepayment penalties and clear portfolio options.

Information on this page is for educational purposes only and is not financial advice. Lending programs change and individual circumstances vary—please consult a licensed mortgage professional or financial advisor before making decisions.