Financing a modular home on owned land is easier than you think. Turn your land equity into your dream home.

Saving a big down payment can feel out of reach. If you already own land, its value can change the math—helping you reduce cash down and move faster. This guide explains how lenders size loans using as-completed value (land + home), what LTV/CLTV mean for pricing, and how a construction-to-permanent loan can work with your equity. For the full picture, start with our pillar guide: modular home loan — what qualifies, rate drivers, and lender types.

This post contains affiliate links. If you buy through our links, we may earn a commission at no extra cost to you. Learn more.

Table of Contents

- Financing a Modular Home on Owned Land: Overview

- How Land Equity Works

- As-Completed Value, LTV & CLTV

- Step-by-Step: From Appraisal to Move-In

- Loan Options

- Compare Loan Types (At-a-Glance)

- Paperwork Checklist

- Common Mistakes to Avoid

- Maximize Your Equity

- Land Equity & LTV Calculator

- Frequently Asked Questions

- Conclusion & Next Steps

Financing a Modular Home on Owned Land: Overview (Modular Home Financing)

If you already own land, you’re closer than you think. Lenders count your land’s value when they size the construction-to-permanent loan—often letting your land equity replace part or all of the cash down. Modular homes are changing homebuilding with affordability, speed, and flexibility. Financing a modular build on land you already own is especially advantageous, as your property’s equity can significantly reduce upfront cash needs.

Modular homes can shorten build times thanks to factory-built modules assembled on-site, while streamlined production can cut labor and material waste. You can customize layouts, finishes, and features to match your vision. And the real game-changer? Your land equity may serve as the down payment, minimizing cash outlay and opening doors to stronger terms.

- Equity as down payment: Counts toward the 20% typically required and can sometimes fully replace cash.

- Single-close convenience: One loan for build and mortgage—avoids a second closing, which can reduce costs.

- Factory timelines: Predictable schedules can mean faster occupancy and lower interest accrual.

How Land Equity Works

Land equity is the difference between your land’s current market value and any outstanding loans against it.

Example: If your land is worth $100,000 and you owe $20,000, your equity is $80,000 (80% of the value). This equity can act as a down payment or reduce the loan amount needed, which may lower your interest rate and improve approval odds.

Sarah’s story: Sarah owned a debt-free $120,000 plot in rural Texas. She leveraged her equity to secure a $200,000 construction-to-permanent loan, achieving a 63% LTV and skipping a cash down payment. Her custom modular home was ready in about six months.

As-Completed Value, LTV & CLTV

Heads up: Loan terms, eligibility, and appraisals vary by lender and location. Always consult a licensed lender and verify details on official sources before making decisions.

When modular home financing involves owned land, lenders look at the as-completed value (land + the finished home). Your loan amount ÷ that value = LTV. Add any existing land lien for CLTV. Lower numbers generally mean less risk and can improve pricing.

“Your land’s equity isn’t just dirt; it’s your ticket to potentially lower rates.”

Loan-to-Value (LTV): This ratio compares your loan amount to the total appraised value of the land plus the completed home. Formula: Loan Amount ÷ (Land Value + Home Value). A lower ratio signals less risk, which may lead to better pricing. Combined LTV (CLTV): Includes all loans on the property, such as an existing land mortgage plus a construction loan. Example: $50,000 land loan + $100,000 construction loan on a $300,000 property = 50% CLTV. Many lenders prefer this ratio ≤ 80% on the finished home; strong equity helps you get there.

Appraisals for modular homes use the as-completed approach, where the appraiser estimates the value of land plus improvements (home build) based on comps for similar finished properties. Site prep—like clearing, grading, or utility stubs—can lift the appraised value, as it reduces buyer risk. A pre-appraisal walkthrough with your lender can flag quick wins.

Curious about your monthly payments based on this ratio? Use our Home Affordability Calculator for a quick estimate.

Step-by-Step: From Appraisal to Move-In

Financing on owned land is straightforward with the right approach. Follow these steps to turn your land into a home.

- Appraise Your Land: Hire a professional to determine your land’s current market value, which sets the foundation for your equity calculation.

- Estimate Project Costs: Modular homes typically cost $100,000–$250,000, depending on size, design, and finishes. Site preparation (e.g., foundation, grading) can add costs, while permits and utility hookups vary by city/county. Always include a 10–15% contingency fund for unexpected expenses. Use our free Mortgage Calculator to estimate monthly payments.

- Assess Your Credit: A higher credit score can secure lower interest rates and better terms.

- Compare Lenders & Get Pre-Approved: Seek out lenders experienced in modular or construction loans; pre-approval clarifies your borrowing capacity.

- Choose a Modular Home Builder: Select a reputable builder with modular expertise. Check reviews, verify licensing, and request photos of past projects.

- Submit Application & Close the Loan: Provide all required documents (see checklist below). Funds are disbursed in draws as construction progresses.

- Move In and Refinance (if needed): Once complete, refinance a construction loan into a permanent mortgage if it saves money.

Typical Construction Draw Schedule for Modular Homes

| Milestone | % Draw | Doc Needed |

|---|---|---|

| Foundation Complete | 10–15% | Site inspection photos |

| Modules Set/Installed | 40–50% | Builder invoice + delivery cert |

| Rough-In (MEP) | 20–25% | Progress inspection report |

| Dry-In (Exterior) | 15–20% | Weather-tight certification |

| Final Completion | Balance | Certificate of occupancy |

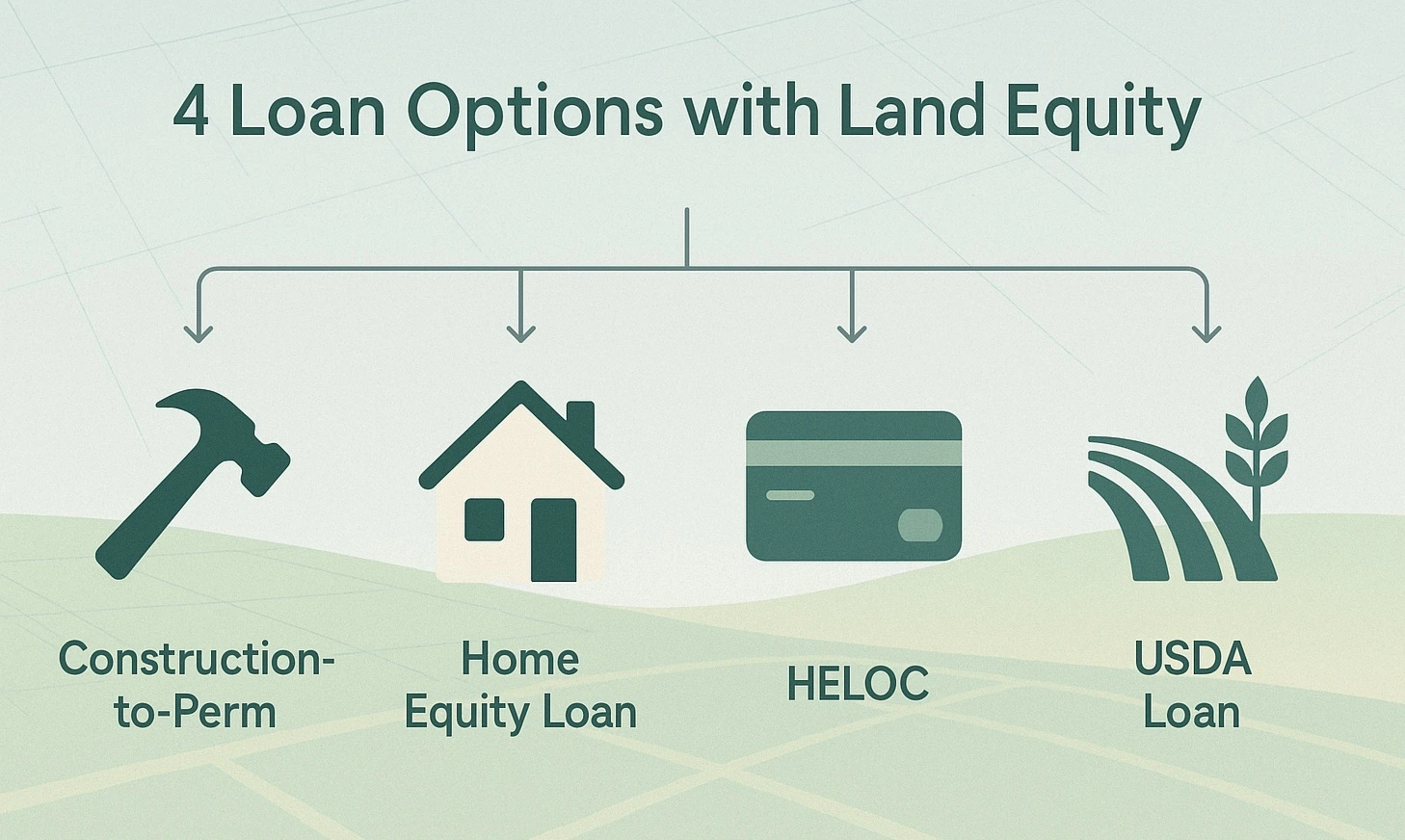

Loan Options

Your land equity opens up several paths for modular home financing on owned land. Here are the top options.

- Construction-to-Permanent Loan: A single loan covers both the build and the final mortgage, with land equity counting as the down payment. Single-close (preferred) vs two-close—single-close can reduce re-underwriting risk but may have higher upfront fees; two-close offers flexibility if plans change. Eligibility and limits vary. Learn more about standards at HUD’s Office of Manufactured Housing Programs.

- Home Equity Loan: Borrow a fixed lump sum against your land’s value, offering predictable payments for construction costs.

- HELOC (Home Equity Line of Credit): A flexible credit line lets you draw funds as needed, useful for phased expenses.

- USDA Loan (Rural Areas): Some lenders offer USDA single-close construction. Eligibility and limits vary by location and program updates. Check eligibility at USDA Single-Family Housing Programs or use the USDA Property Eligibility map.

What Is a Construction-to-Permanent Loan?

A construction-to-permanent loan rolls your build financing into a lasting mortgage at completion. Many borrowers prefer a single-close construction to avoid a second underwriting and closing. Keep your LTV near 80% by leveraging land equity and realistic costs; lender requirements vary.

USDA Single-Close Construction Loan (USDA construction loan)

A USDA construction loan can fund up to 100% in eligible rural projects depending on program and underwriting. If your land already has equity, your CLTV can remain conservative while benefiting from reduced or zero-down requirements; check current lender offerings.

Case Study: No-Cash-Down with Land Equity

Meet Alex, a teacher in Oregon with a $150k debt-free lot. Home build: $220k. As-completed value: $370k. Equity: $150k (40% of total). Loan: $220k construction-to-permanent.

Draw Schedule: 15% foundation ($33k), 50% install ($110k), 20% MEP ($44k), 15% final ($33k).

Final CLTV: 59%—well under 80%. Outcome: Zero cash down possible, 5.25% rate (illustrative), move-in at ~4 months. Tip: Pre-clearing the lot boosted the appraisal.

Compare Loan Types (At-a-Glance)

Illustrative ranges; lenders/markets change often. Always confirm current rates/fees with your lender.

| Loan Type | Best For | Equity Needed | Typical Rates* |

|---|---|---|---|

| Construction-to-Perm | Full build + mortgage | ~20%+ | Varies by market |

| Home Equity Loan | Lump sum funding | ~15–25% | Varies by market |

| HELOC | Flexible borrowing | ~15–25% | Varies by market |

| USDA Loan | Rural landowners | Program-dependent | Program-dependent |

Paperwork Checklist

Prepare these documents to help ensure a smooth loan application: your land deed or title, a recent land appraisal, modular home plans and specifications, builder contract with timeline, construction permits, proof of income (W-2s, pay stubs), tax returns (past 2 years), bank statements, insurance policies (home, builder’s risk), and land survey (boundaries, easements). For more on budgeting these costs, see our modular home loan guide.

Common Mistakes to Avoid

Don’t let these pitfalls derail your modular home financing:

- Budget & Permits: Underestimating site work, permits, and utility hookups can add thousands—pad 10–15% and confirm timelines with local officials.

- Builder & Zoning: Skipping pre-approval risks planning beyond budget. Verify modular experience and zoning early.

- Shopping & Cushion: Not comparing lenders means missing better terms; forgetting a contingency fund leaves you exposed.

Maximize Your Equity

“Small land upgrades can unlock bigger financing power.”

- Clear your land: remove debris to boost curb appeal and appraisal value.

- Add utilities: access to water/electricity can increase your land’s worth.

- Pay down debt: reducing land loans maximizes usable equity.

Land Equity & LTV Calculator

Not sure how much equity you have? Use this interactive tool to see your land equity and LTV in seconds. Values are estimates in US dollars (USD) and update as you type or slide.

Frequently Asked Questions

Conclusion & Next Steps

Financing a modular home on land you own can leverage your property’s value to reduce down payments, secure better terms, and speed up your path to homeownership. With the right loan, preparation, and builder, your dream home is closer than you think.

Ready to build? 1) Run the equity calculator, 2) Check affordability with our free Home Affordability Calculator, 3) Shortlist 2–3 lenders that do single-close construction.

Disclaimer. Educational only—not financial, tax, or legal advice. Rates, fees, eligibility, and program availability change by lender and location. Examples and calculator outputs are illustrative. Verify zoning/codes with local authorities and speak with a licensed lender. For program details, see official HUD/USDA resources.